Understanding legality when running a company is important but often overlooked by founders. This is understandable, though, as laws and regulations are often complex and daunting… at least for those who did not go to law school.

To help you understand the fundamentals of commercial law, Charlene Sell and Phoebe Davis from Wynn Williams have put together a series of articles that uncovers different phases of business from a legal perspective, and discuss what founders need to keep in mind when their company moves through each stage of the business lifecycle.

Without further due, enter Wynn Williams…

Wynn Williams is the official legal partner of Te Ōhaka who provides legal support to high-growth startups at Te Ōhaka.

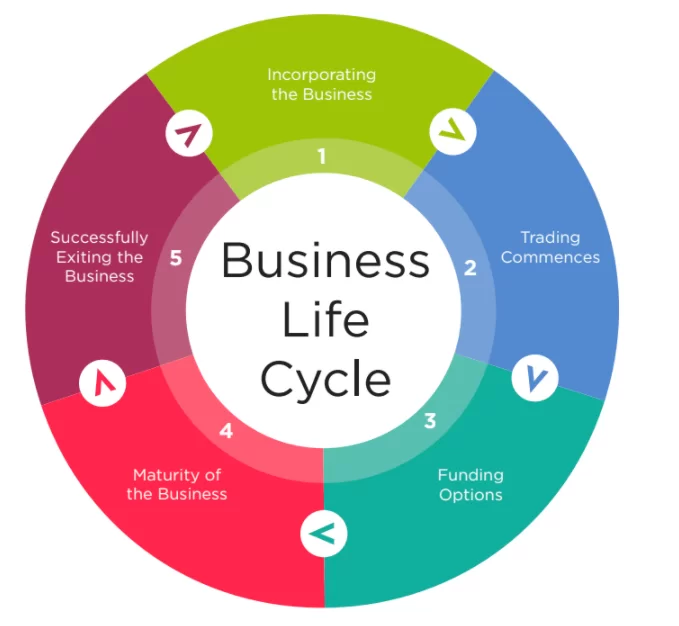

Navigating the legalities of owning and running a business can be tricky, especially as there are so many different aspects to consider. To assist with this, every couple of weeks over the course of 2020 we shall be producing articles to help guide business owners through the life cycle of a business. The areas we shall cover are:

1. Incorporating the Business

2. Trading Commences

3. Funding Options

4. Maturity of the Business

5. Successfully Exiting the Business

The aim is to provide business owners with easy to read bitesize information on a number of key areas that are likely to affect their business.

Chapter 1. Business Structure

An important question for founders to consider is the structure of the business. There are different ways to set up a business, each with different legal and financial obligations.

Businesses in New Zealand are generally sole traders, limited companies or partnerships. What does each one mean?

Sole Trader

A sole trader is a person who is the exclusive owner of a business. A sole trader may apply for a New Zealand Business Number, a unique identifier which helps speed up interactions with Government, suppliers and customers, and other businesses. Operating as a sole trader is simple – there is no need for legal documentation, nor to go through a legal process or register a business with a government agency and there are minimal ongoing administrative requirements. A sole trader has full control of the business. The major drawback is that the sole trader is liable for all business losses and has unlimited personal liability.

Limited Company

A limited company is incorporated under the Companies Act 1993. With a limited liability company, the liability of each shareholder is limited to any amount of unpaid share capital in respect of the shares they own. A company has a separate legal personality and is deemed to have all the rights and powers of a natural person. A company must have at least one director, and at least one director must be resident in New Zealand or Australia. Directors have an obligation to comply with the duties set out in the Companies Act 1993. A company must have at least one shareholder, but there is no limitation on the number of shareholders a company may have, and the shareholders do not need to be based in New Zealand.

A company may adopt a constitution, which is a document providing for variations to the default position provided by a number of provisions under the Companies Act 1993 and which can empower the company to do certain things which can only be done under a constitution.

If there is more than one shareholder, the shareholders should enter into a shareholders’ agreement, which is a contract between the shareholders governing the business. The shareholders’ agreement may specify each shareholder’s role in the company, how significant business decisions should be made, how a shareholder’s shares should be dealt with if that

shareholder exits the company, how funding will be obtained, how disputes will be resolved, how exits will be managed and obligations on shareholders where there is a potential sale of the entire company.

The main advantage of a limited company structure is that the legal liabilities of the business are separated from the shareholders’ personal assets. A company can be incorporated quickly and inexpensively online. The main disadvantage of a limited company structure is the ongoing reporting and record-keeping obligations.

Partnerships

Two or more people or companies may act as a general partnership, by carrying on business in common with a view to profit. Unincorporated partnerships are regulated by the Partnership Act 1908 and the common law. They are not required to have a written partnership agreement, there is no need to incorporate or register the arrangement with a third-party authority, and there are no specific administration requirements. They are not a separate legal entity, and each partner can be held liable for all of the liabilities of the partnership.

Limited partnerships are governed by the Limited Partnerships Act 2008 and must be registered with the Companies Office.

They are a separate legal entity and must consist of at least one general partner and one limited partner. The general partner manages the limited partnership and is liable for the debts and liabilities of the partnership (it is typical for a general partner to itself be a limited liability entity such as a company). Limited partners are restricted from participating in the management of the limited partnership and their liability is limited. A limited partnership must have a written partnership agreement, which is akin to a shareholders’ agreement.

Summary

While there are no great barriers in New Zealand to using any of these business structures, it is important to get it right as the structure you choose can impact your ability to grow or sell the business. In considering which structure, it is always key to obtain tax advice before proceeding.

We hope you find these articles useful if you have questions on any of the information provided, don’t hesitate to contact Charlene Sell or Phoebe Davies, details below.

About authors

Phoebe Davies

Partner

P: +64 3 353 0221

M: +64 27 414 9825

E: [email protected]

Phoebe advises on a wide range of corporate and commercial law, including overseas investments, mergers and acquisitions, corporate structuring, shareholders’ agreements, corporate governance and commercial contracts.

Phoebe acts for clients in a broad range of industry sectors with specialist knowledge in the agribusiness and consumer finance sectors. In addition to Phoebe’s New Zealand experience, she has worked for international firms in both London and Birmingham in the United Kingdom, and is qualified to practice law in both New Zealand and England & Wales.

Charlene Sell

Partner

P: +64 3 379 7622

M: +64 27 685 5653

E: [email protected]

Charlene advises business owners and managers on how to structure their businesses and how to resolve their day-to-day issues. Her expertise includes business acquisitions and sales, drafting and providing advice on commercial contracts and terms of trade, advising on export arrangements, dealing with employment matters and protecting clients’ brands.

Charlene also advises business owners with structuring their personal affairs, including establishing family trusts and advising on succession planning.